As we referenced in last month’s newsletter, Tideland is poised to implement a base rate increase effective with all bills rendered beginning March 1, 2026.

The last time Tideland EMC implemented a base rate increase was March 2020 following a base rate decrease in July 2014. Immediately after the March 2020 rate change, all members benefited from a 36-month wholesale power cost adjustment (WPCA) credit to reflect energy costs that were lower than our published rates.

In 2023, the WPCA reverted to a per kilowatt hour (kWh) charge and for that year added, on average, $1.91 to each 1,000 kWh of energy you purchased from the co-op. In 2024, the average monthly WPCA added $2.48 to each 1,000 kWh you used.

By the end of 2025, the WPCA had quadrupled with members paying $11.94 more per 1,000 kWh billed during the month of December. At press time we estimated a February 2026 WPCA of $13.00 per 1,000 kWh.

While the WPCA can reflect both rising and falling energy costs, there comes a point where the pricing trajectory is clear. You can see that reflected in the chart above right. With no anticipation of lower power costs in the foreseeable future, Tideland will roll today’s WPCA charge into new base rates.

Because Tideland predominantly serves residential accounts, this discussion will largely focus on residential rates 1 and 2. Let’s first look at the energy costs (per kWh) for those rates.

For the month of December, rates 1 and 2 were billed 12.684¢ per kilowatt hour. That is the current winter base rate of 11.49¢ plus December’s WPCA charge of 0.01194¢. The new winter base rate for energy will be 12.746¢ per kWh. So while the effective base rate increase from March 2020 to March 2026 is 10.93%, the per kWh change between December 2025 and March 2026 will be just shy of one half of one percent (0.49%).

Where we did factor in a higher percent increase was in the area of the basic facilities charge. The fixed residential overhead basic facilities fee will move from $27.50 to $32.00. Residential underground will move from $29.80 to $34.30.

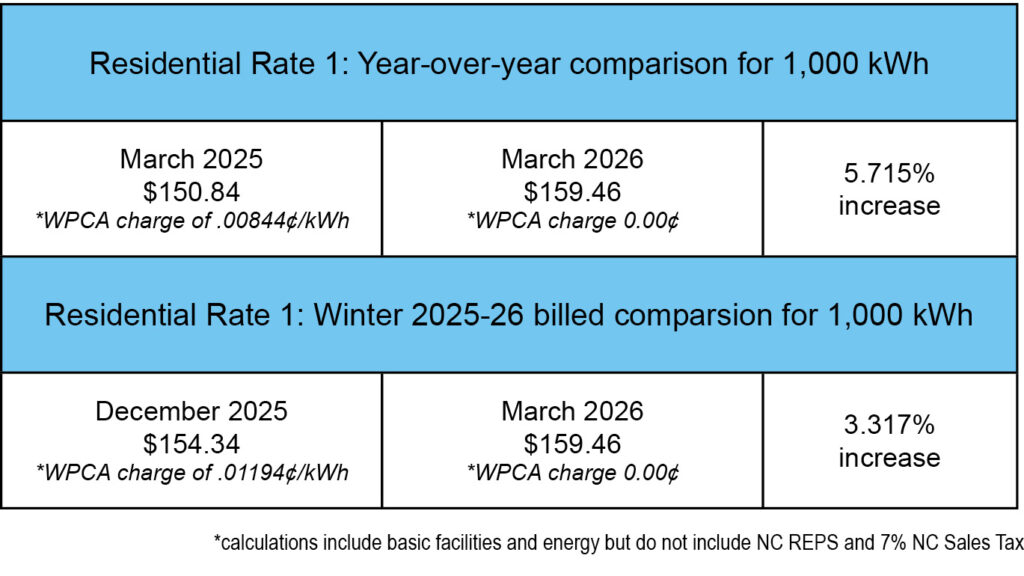

When we look at the all in cost comparison (energy and facilities) for residential rate 1 based on 1,000 kWh in winter (see directly above), the new rates represent a 5.715% increase year-over-year for March, and a 3.317% increase from December 2025 to March 2026.

What is driving costs?

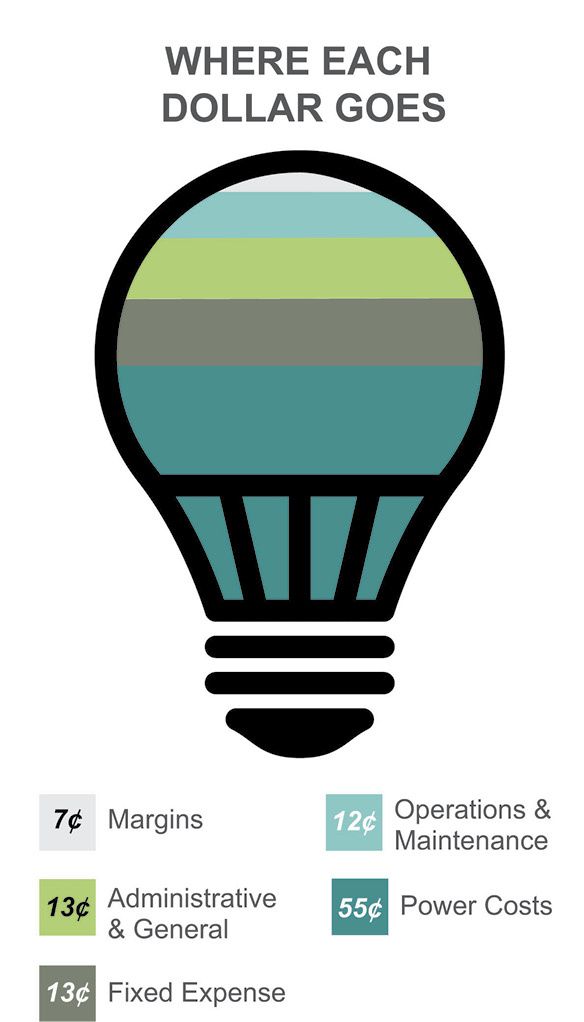

The graphic to your left is taken from our most recent annual report. You can see that power costs and system operations and maintenance make up 67% of our annual expenses.

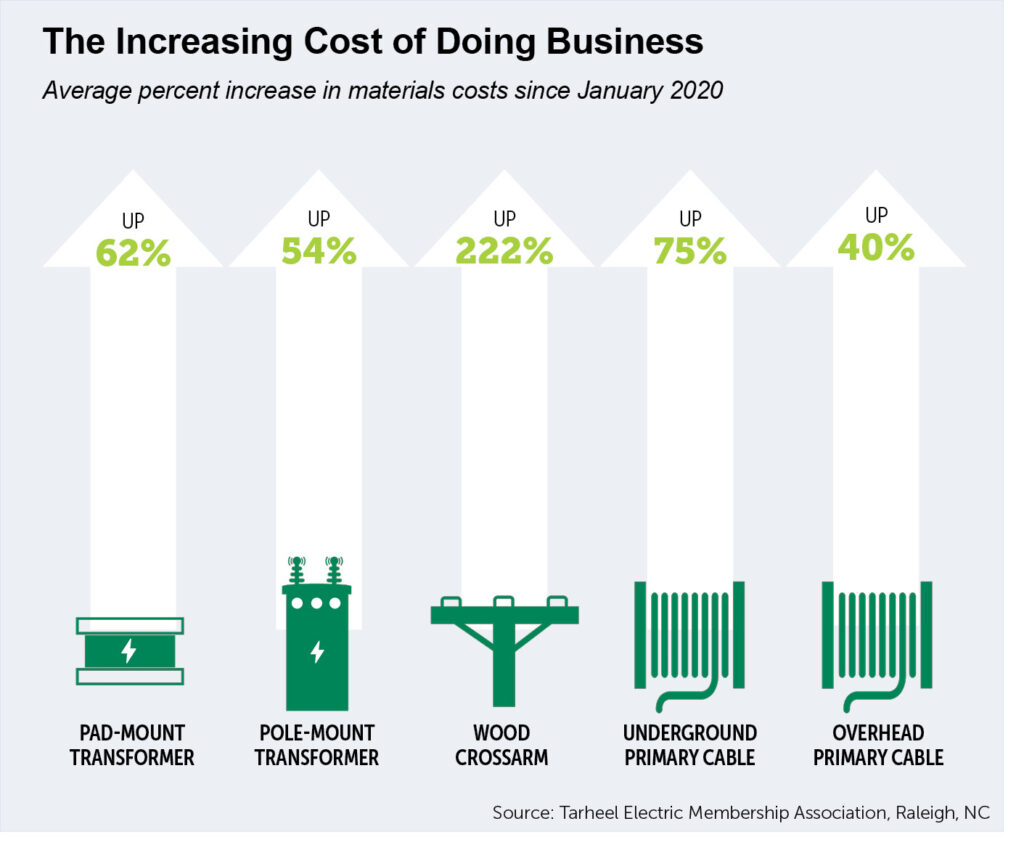

In the area of system operations and maintenance, we have been confronted with significant inflationary pressures for many of the most basic materials we use on a daily basis (see graphic below). The reasons are varied starting with supply chain disruptions that began during the pandemic. Add to that a multitude of devastating storms like Hurricane Helene and western wildfires that left electric utility materials warehouses scrambling. Southern pine beetles, drought and fire have devastated many of the forests that produce power poles.

A concerted effort to finally address the nation’s aging electric utility infrastructure flooded the industry with dollars that further exasperated supply chains and prices. Large transformers can now take up to four years to acquire with smaller transformers back-ordered as much as two years. These and other factors had the makings of a perfect storm for the electric utility construction industry.

However, the most significant driver of our base rate increase is the rising cost of wholesale power which consists of generation and transmission expense. The industry has experienced significant weather driven price volatility in recent years. Even if a weather event such as a polar vortex does not impact Tideland territory directly, because electricity is managed as a regional supply across multiple states, what happens in Maryland or South Carolina can impact our cost for power. And these costs are not in our rear-view mirror. A recent analysis by one of our power market partners anticipates a 45% increase in the cost of constructing new natural gas generating facilities in the next few years.

Make no doubt about it, an abundance of new generating assets will be needed to meet projected energy demands that continue to outpace national energy demand forecasts.

If you were a member of Tideland in the 80s and 90s, you may remember our load management program. A favorite tag line was “Beat the Peak.” The program addressed a costly imbalance between generating supply and market demand. We were incredibly successful with the program, achieving up to $1.3 million in annual wholesale power cost savings in the mid-90s. It was during those years that we first rolled out our residential time-of-use rate.

Then demand for electricity in the U.S. decelerated in 2000 and Beat the Peak efforts were shelved as wholesale power cost rate structures substantially changed.

Fast forward twenty-five years and peak pricing is once again driving wholesale power costs. While adding generating assets to the mix is a necessity, that too comes with increased costs and significant lag time. Therefore, upward pressure on electric rates will continue for the foreseeable future.

Read the rest of the series

This article is first In a three-part series. Read “What Tideland is doing to control rates” next to learn more.

More news from Tideland EMC

Geospring HPWH returns

August rights-of-way maintenance schedule

Billing cycle blues for some while peak reduction efforts benefit all

A message to members from Paul Spruill, General Manager & CEO